Filed under: Uncategorized

Below is some of the key budget changes affecting individuals and small business.

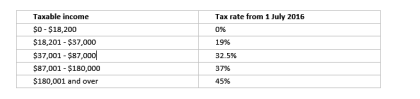

Personal tax cuts for middle income earners

Date of effect 1 July 2016

The 32.5% personal income tax threshold will increase from $80,000 to $87,000 from 1 July 2016. The new tax rates from 1 July 2016 would be as follows:

These tax rates exclude the Medicare Levy and the 2% debt tax on high-income earners over $180,000 which will come to an end on 30 June 2017.

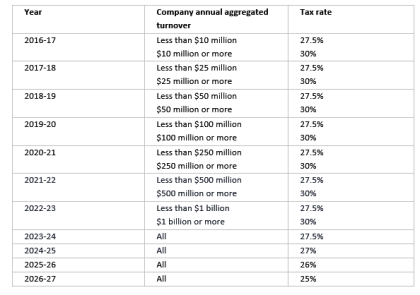

Reducing the company tax rate to 25%

Date of effect Progressively from 2016-17

The company tax rate will be reduced to 25% over 10 years. The reduction will initially target companies with a turnover less than $10 million, then gradually increase access:

Franking credits will still be calculated with reference to the amount of tax paid by the company paying the dividends.

Small business entity threshold jumps to $10m

Date of effect 1 July 2016

In a significant win for business, the small business entity turnover threshold will increase from $2 million to $10 million from 1 July 2016. The reform will give a greater number of businesses access to a range of tax concessions such:

• The lower small business corporate tax rate (27.5%);

• Simplified depreciation rules including an immediate write-off for assets costing less than $20,000 that are acquired by 30 June 2017 and depreciation pooling provisions;

• Simplified trading stock rules;

• A different method of calculating PAYG instalments;

• The option of accounting for GST on a cash basis;

• FBT exemptions (this would start from 1 April 2017); and

• A trial system of using a simpler business activity statement.

The current $2 million turnover threshold will be retained for access to the small business CGT concessions and access to the unincorporated small business tax discount will be limited to entities with turnover less than $5 million.

Lifetime cap on non-concessional contributions

Date of effect 7.30 pm (AEST) on 3 May 2016

Applies to all non-concessional contributions made on or after 1 July 2007

A lifetime $500,000 non-concessional contributions cap will be introduced from Budget night.

The current system of annual non-concessional contributions of up to $180,000 per year (or $540,000 every three years for individuals aged under 65), will be replaced with this new lifetime cap.

The lifetime cap will take into account all non-concessional contributions made on or after 1 July 2007 and will commence at 7.30 pm (AEST) on 3 May 2016. Contributions made before commencement will not result in an excess. However, excess contributions made after commencement will need to be removed or will be subject to penalty tax. The cap will be indexed to average weekly ordinary time earnings.

After-tax contributions made into defined benefit accounts and constitutionally protected funds will be included in an individual’s lifetime non-concessional cap. If a member of a defined benefit fund exceeds their lifetime cap, ongoing contributions to the defined benefit account can continue but the member will be required to remove, on an annual basis, an equivalent amount (including proxy earnings) from any accumulation account they hold. The amount that could be removed from any accumulation accounts will be limited to the amount of non-concessional contributions made into those accounts since 1 July 2007. Contributions made to a defined benefit account will not be required to be removed.

The lifetime cap is available up to age 74.

Concessional contributions cap reduced

Date of effect 1 July 2017

The current concessional contributions cap will reduce to $25,000 from 1 July 2017.

From 1 July 2017, the Government will include notional (estimated) and actual employer contributions in the concessional contributions cap for members of unfunded defined benefit schemes and constitutionally protected funds. Members of these funds will have opportunities to salary sacrifice commensurate with members of accumulation funds. For individuals who were members of a funded defined benefit scheme as at 12 May 2009, the existing grandfathering arrangements will continue.

Tax Exemption on Transition to Retirement Income Stream Earnings removed

Date of effect 1 July 2017

The tax exemption on the earnings of assets supporting Transition to Retirement Income Streams will be removed from 1 July 2017. The rule that allows individuals to treat certain superannuation income stream payments as lump sums for tax purposes will also be removed.

30% tax on super for high income earners

Date of effect 1 July 2017

At present, individuals with combined income and superannuation contributions of more than $300,000 pay an additional contributions tax of 15% on concessional contributions. From 1 July 2017, this income threshold will reduce to $250,000.

The lower Division 293 income threshold will also apply to members of defined benefit schemes and constitutionally protected funds currently covered by the tax. Existing exemptions (such as State higher level office holders and Commonwealth judges) for Division 293 tax will be maintained.

Tax free super balances capped at $1.6m

Date of effect 1 July 2017

A new $1.6 million cap will apply to how much can be transferred into a retirement phase account. Earnings on amounts within the account will continue to be tax-free. Transfers in excess of this $1.6 million cap (including earnings on these excess transferred amounts) will be taxed in a similar way to the tax treatment that applies to excess non-concessional contributions.

Where an individual accumulates amounts in excess of $1.6 million, they will be able to maintain this excess amount in an accumulation phase account (where earnings will be taxed at the concessional rate of 15%).

Members already in the retirement phase with balances above $1.6 million will be required to reduce their retirement balance to $1.6 million by 1 July 2017. Excess balances for these members may be converted to superannuation accumulation phase accounts.

The amount of cap space remaining for a member seeking to make more than one transfer into a retirement phase account will be determined by apportionment.

Commensurate treatment for members of defined benefit schemes will be achieved through changes to the tax arrangements for pension amounts over $100,000 from 1 July 2017.

Tax deductions on super contributions expanded

Date of effect 1 July 2017

All individuals up to age 75 will be able to claim an income tax deduction for personal superannuation contributions from 1 July 2017. This effectively allows all individuals, regardless of their employment circumstances, to make concessional superannuation contributions up to the concessional cap – partially self employed, employees whose employers don’t offer salary sacrifice arrangements, etc.

This is a sensible move which means that it will no longer be necessary for individuals to pass a 10% test in order to be able to claim a deduction for personal superannuation contributions. Currently, an individual can only claim a deduction for personal contributions where less than 10% of their adjusted income for the year relates to employment activities. The 10% test can make it difficult for people who have started their own business to make deductible superannuation contributions where they also have part-time work.

Notes

Please note there were many other tax changes announced on budget night. If you would like to discuss your individual circumstances in more detail please contact me.

The material and contents provided in this publication are informative in nature only. It is not intended to be advice and you should not act specifically on the basis of this information alone. If expert assistance is required, professional advice should be obtained.

Leave a Comment so far

Leave a comment